I. Introduction

Most people think they understand their financial situation until they actually sit down and examine it. You might know how much you earn and have a rough idea of what you spend, but when asked about your overall financial health, the answer often becomes fuzzy. This confusion stems from a common mistake: viewing money as isolated numbers rather than as part of a dynamic system.

Money doesn’t exist in silos. It moves. It comes in, flows out, accumulates, and sometimes disappears faster than expected. This movement this continuous cycle is what we call money flow.

Understanding money flow means seeing how income, expenses, and net worth interact over time. These three components are not separate they are deeply interconnected. Income fuels your spending, spending affects your savings, and savings ultimately determine your net worth.

Thesis: When you understand income, expenses, and net worth together as parts of a single system, you gain a complete and accurate picture of your financial health and the power to improve it.

II. The Big Picture: What “Money Flow” Really Means

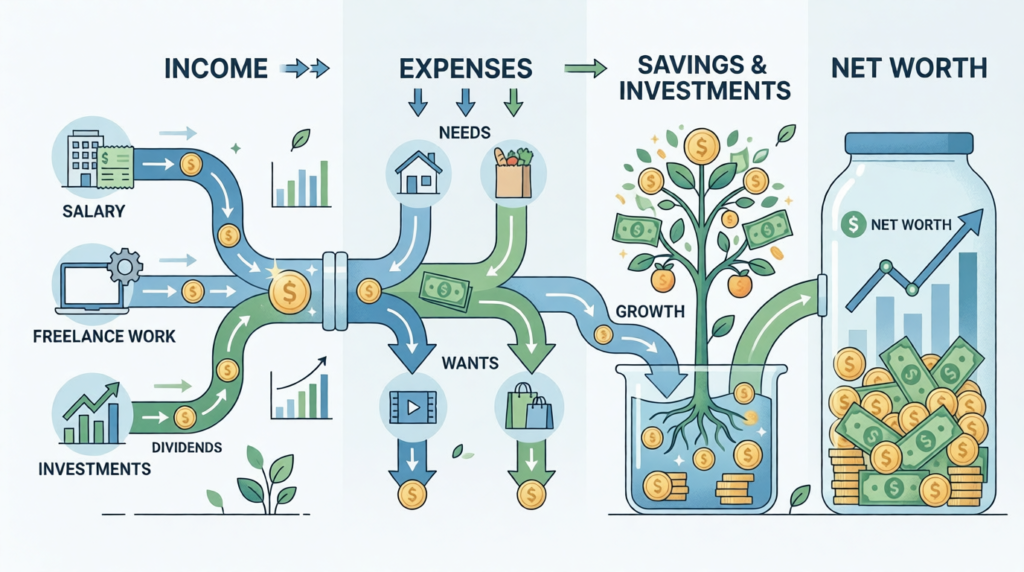

At its core, money flow refers to the movement of money into and out of your life over time.

- Inflows: Income from work, investments, or other sources

- Outflows: Expenses, bills, debt payments, and discretionary spending

Cash Flow vs. Net Worth

It’s crucial to distinguish between two related but different concepts:

- Cash Flow: The short-term movement of money (monthly or daily)

- Net Worth: The long-term accumulation of wealth (what you own minus what you owe)

Cash flow tells you how money behaves right now. Net worth tells you where you stand overall.

The Pipeline Analogy

Imagine your finances as a system of pipes:

- Income is the water entering the system

- Expenses are leaks or outlets

- Savings and investments are reservoirs

- Net worth is the total water stored

If too much water leaks out (expenses), your reservoir never fills. If more water flows in than out, the system strengthens over time.

This simple analogy captures a powerful truth: financial health depends on flow, not just volume.

III. Income: The Starting Point

A. Definition of Income

Income is any money you receive over a period of time. It is the fuel that powers your financial system.

Without income, there is no flow only depletion.

B. Types of Income

Not all income is created equal. Understanding the types helps you build stability and growth.

1. Active Income

This is money earned through direct effort:

- Salaries and wages

- Freelance work

- Contract or gig income

Active income requires your time and energy. If you stop working, it usually stops too.

2. Passive Income

Passive income is generated with minimal ongoing effort:

- Rental income

- Royalties

- Business systems that run without daily involvement

While “passive” often requires upfront work, it creates long-term leverage.

3. Portfolio Income

This comes from investments:

- Dividends from stocks

- Interest from bonds or savings

- Capital gains from asset appreciation

Portfolio income is a key driver of long-term wealth.

C. Gross vs. Net Income

A common mistake is focusing on gross income instead of what you actually receive.

- Gross Income: Total earnings before taxes and deductions

- Net Income: Take home pay after taxes, insurance, and other deductions

Your financial decisions should always be based on net income, not gross.

D. Income Stability and Growth

Fixed vs. Variable Income

- Fixed income: Predictable (salary)

- Variable income: Fluctuates (freelance, commissions)

Stability matters. Predictable income makes planning easier.

Importance of Diversification

Relying on a single income source is risky. Diversifying income streams provides resilience against job loss or market shifts.

Strategies for Increasing Income

- Skill Development

Learning high demand skills can significantly increase earning potential. - Side Hustles

Freelancing, online businesses, or part-time work can supplement income. - Investing

Over time, investments can generate income independent of your labor.

Income is the starting point but it’s only the beginning of the story.

IV. Expenses: Where the Money Goes

A. Definition of Expenses

Expenses are all the ways money leaves your system:

- Bills

- Purchases

- Financial obligations

Every dollar spent is a dollar that cannot be saved or invested.

B. Categories of Expenses

1. Fixed Expenses

These are consistent and predictable:

- Rent or mortgage

- Insurance

- Loan payments

They form the foundation of your cost structure.

2. Variable Expenses

These fluctuate:

- Groceries

- Entertainment

- Utilities

Variable expenses offer flexibility but also risk overspending.

3. Periodic or Irregular Expenses

Often overlooked, these include:

- Car repairs

- Medical bills

- Annual subscriptions

Ignoring these can disrupt your financial stability.

C. Needs vs. Wants

Understanding this distinction is critical.

- Needs: Essentials (housing, food, transportation)

- Wants: Non-essential (luxuries, upgrades, entertainment)

The challenge is psychological. Many “wants” feel like needs due to habits, social pressure, or emotional triggers.

Behavioral Influences on Spending

Spending is rarely rational. It is influenced by:

- Emotions (stress, boredom)

- Social comparison

- Marketing and convenience

Recognizing these influences helps you make more intentional decisions.

D. Tracking and Managing Expenses

Budgeting Methods

- 50/30/20 Rule

- 50% needs

- 30% wants

- 20% savings

- Zero-Based Budgeting

Every dollar is assigned a purpose. - Envelope System

Physical or digital “envelopes” limit spending categories.

Common Pitfalls

- Lifestyle Inflation: Spending increases as income rises

- Subscription Creep: Small recurring charges add up over time

Managing expenses is not about restriction it’s about alignment with your goals.

V. Cash Flow: The Relationship Between Income and Expenses

A. Positive vs. Negative Cash Flow

Cash flow is the difference between income and expenses.

- Positive Cash Flow: Income > Expenses

- Negative Cash Flow: Expenses > Income

Positive cash flow creates opportunity. Negative cash flow creates stress.

B. Why Cash Flow Matters

Cash flow determines:

- Your ability to save

- Your ability to invest

- Your financial flexibility

Even high earners can struggle if their expenses outpace income.

C. Improving Cash Flow

There are two main levers:

1. Increase Income

- Seek raises or promotions

- Add income streams

- Invest for returns

2. Reduce Expenses

- Cut unnecessary costs

- Optimize recurring bills

- Avoid wasteful spending

Short-Term vs. Long-Term Adjustments

- Short-term: Cut discretionary spending

- Long-term: Increase income or reduce fixed expenses

The best strategy usually involves both.

VI. Net Worth: The Financial Snapshot

A. Definition of Net Worth

Net worth is the ultimate measure of financial position:

Net Worth = Assets – Liabilities

It answers a simple question: What do you truly own?

B. Assets Explained

1. Liquid Assets

- Cash

- Checking and savings accounts

These provide immediate access and flexibility.

2. Investments

- Stocks

- Bonds

- Retirement accounts

These grow over time and generate wealth.

3. Physical Assets

- Real estate

- Vehicles

- Valuable possessions

These may appreciate or depreciate.

C. Liabilities Explained

1. Short-Term Debt

- Credit cards

- Personal loans

Often high interest and financially draining.

2. Long-Term Debt

- Mortgages

- Student loans

These can be strategic but still impact net worth.

D. Why Net Worth Matters

Net worth reflects:

- Financial progress

- Wealth accumulation

- Long-term stability

Unlike income, which is temporary, net worth represents lasting value.

VII. How It All Connects

A. The Flow Cycle

The financial system follows a simple cycle:

Income → Expenses → Savings/Investments → Net Worth

Each step influences the next.

- Higher income increases potential savings

- Lower expenses free up more cash

- Savings and investments build assets

- Assets increase net worth

B. The Time Dimension

- Short-term (daily/monthly): Cash flow

- Long-term (years/decades): Net worth

Short-term decisions compound into long-term outcomes.

C. Feedback Loops

Positive Loop

- Strong cash flow

- Increased investing

- Growing net worth

Negative Loop

- Poor cash flow

- Increasing debt

- Declining net worth

Your financial trajectory depends on which loop you reinforce.

VIII. Common Misconceptions

“High Income Equals Wealth”

Many high earners live paycheck to paycheck. Without control over expenses, income alone doesn’t create wealth.

“Cutting Expenses Is Enough”

Frugality helps but there’s a limit. Income growth is equally important.

“Net Worth Only Matters for the Rich”

Everyone has a net worth, even if it’s negative. Tracking it provides clarity and direction.

Ignoring Debt

Debt is often underestimated. It directly reduces net worth and can severely impact cash flow.

IX. Practical Steps to Take Control

A. Assess Your Current Situation

Start with clarity:

- Calculate net income

- Track expenses

- Determine net worth

You can’t improve what you don’t measure.

B. Build a Simple System

Complexity leads to inconsistency. Keep it simple:

- Track income and spending regularly

- Automate savings and investments

- Review progress monthly

Automation reduces friction and improves consistency.

C. Set Financial Goals

Short-Term Goals

- Build an emergency fund

- Pay off small debts

Medium-Term Goals

- Save for major purchases

- Reduce significant debt

Long-Term Goals

- Retirement

- Financial independence

Goals give direction to your money flow.

X. Conclusion

Money is not just something you earn or spend it’s something that moves through a system. Income, expenses, and net worth are not isolated concepts; they are interconnected parts of a larger financial ecosystem.

Understanding this system changes everything. Instead of reacting to money, you begin to control it.

You don’t need perfection. You need consistency.

Small improvements spending a little less, earning a little more, investing regularly compound over time into meaningful financial strength.

In the end, mastering money flow is not about complexity. It’s about awareness, intention, and steady progress.