I. Introduction

Managing money can feel overwhelming, especially if you’ve never created a budget before. Between bills, unexpected expenses, and trying to enjoy life, it’s easy to lose track of where your money is going. That’s exactly why budgeting matters it gives you clarity, control, and confidence over your finances.

A good budget helps you:

- Understand your spending habits

- Reduce financial stress

- Work toward goals like saving, investing, or paying off debt

Without a plan, money tends to disappear quickly, often leaving you wondering where it all went.

Common Budgeting Challenges

Many people struggle with budgeting for a few key reasons:

- Complexity: Some budgeting systems are too detailed and hard to maintain

- Inconsistency: People start strong but stop tracking after a few weeks

- Lack of structure: Without a clear framework, it’s easy to overspend

If you’ve ever tried budgeting and given up, you’re not alone. The good news is you don’t need a complicated system to succeed.

A Simpler Approach: The 50/30/20 Rule

The 50/30/20 rule is a straightforward budgeting method that divides your income into three main categories:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

It’s flexible, easy to understand, and works well for beginners.

What You’ll Learn

In this guide, you’ll learn:

- How the 50/30/20 rule works

- How to calculate your income

- How to categorize your expenses

- Practical tips to stick to your budget

By the end, you’ll be ready to build a simple, effective budget that actually works.

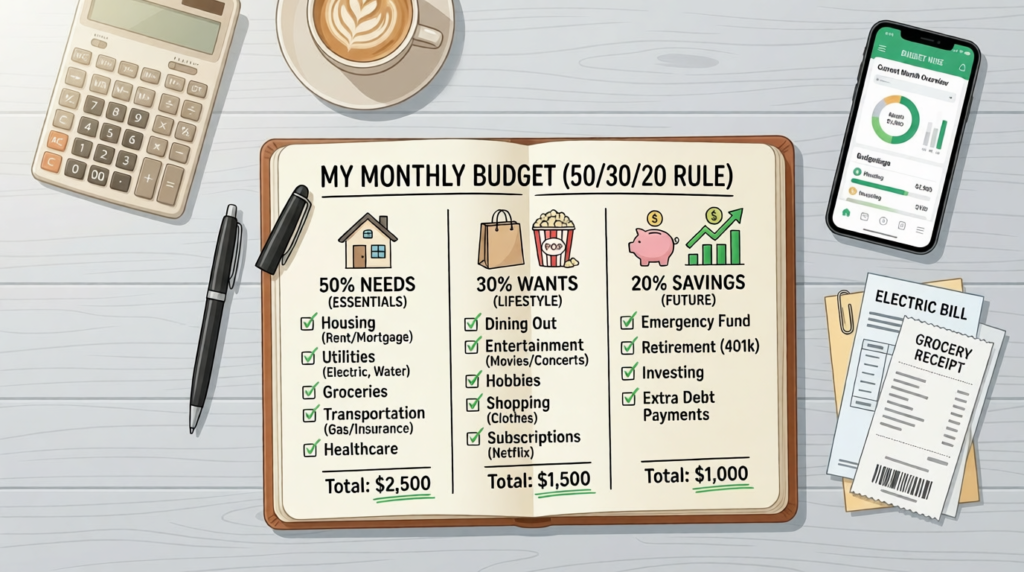

II. What Is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting framework that helps you divide your after tax income into three categories:

- 50% Needs: Essential expenses

- 30% Wants: Lifestyle and discretionary spending

- 20% Savings & Debt Repayment: Financial goals

Why This Rule Works

The strength of this method lies in its simplicity. Instead of tracking dozens of categories, you only focus on three. This makes it easier to follow and maintain over time.

It’s also flexible. Whether you earn a modest income or a higher salary, you can adapt the percentages slightly to fit your situation.

Who Is It Best For?

The 50/30/20 rule is ideal for:

- Beginners who are new to budgeting

- People who want a simple system

- Moderate income earners

- Anyone looking to build better financial habits

III. Step 1: Calculate Your After Tax Income

Before you can create a budget, you need to know how much money you actually have available to spend.

What Is After Tax Income?

After tax income (also called net income) is the amount you take home after taxes and deductions. This is the money that hits your bank account.

What to Include

Make sure to include all income sources:

- Salary (after taxes)

- Freelance or side income

- Bonuses or commissions

- Any other consistent income streams

Monthly vs. Biweekly Income

If you’re paid monthly, your calculation is simple. If you’re paid biweekly (every two weeks), multiply your paycheck by 26 (weeks) and divide by 12 to get a monthly average.

Tools to Help

You can use:

- Pay stubs

- Bank statements

- Budgeting apps

- Simple spreadsheets

Example Calculation

Let’s say:

- Monthly take home salary: $3,000

- Side income: $500

Total after tax income = $3,500 per month

This is the number you’ll use for your budget.

IV. Step 2: Allocate 50% to Needs

The first category covers essential expenses things you must pay to live and work.

A. What Counts as “Needs”

Needs include:

- Housing (rent or mortgage)

- Utilities (electricity, water, internet)

- Groceries

- Transportation (gas, public transit)

- Insurance (health, car, home)

- Minimum debt payments

These are non-negotiable expenses.

B. Needs vs. Non-Needs

A helpful question to ask:

“Is this essential for survival or earning income?”

Some expenses fall into a gray area:

- A basic phone plan = need

- A premium unlimited plan = want

Be honest when categorizing.

C. What If You Exceed 50%?

Many people find their needs exceed 50%, especially in high-cost areas.

Common reasons:

- Expensive rent

- High debt payments

- Cost of living

Strategies to Reduce Needs

- Downsize your housing

- Refinance loans

- Shop around for insurance

- Cut unnecessary “needs”

Even small reductions can make a big difference.

V. Step 3: Allocate 30% to Wants

This category is for non-essential spending that improves your quality of life.

A. What Counts as “Wants”

Wants include:

- Dining out

- Entertainment (movies, streaming)

- Travel

- Shopping (clothes, gadgets)

- Hobbies

These are things you enjoy but don’t strictly need.

B. Why Wants Matter

Cutting all fun spending might seem like a good idea, but it often leads to burnout. When people feel deprived, they tend to overspend later.

Including wants in your budget:

- Keeps you motivated

- Helps you stick to your plan

- Creates balance

C. Managing Wants Effectively

To stay in control:

- Prioritize what matters most to you

- Avoid impulse purchases

- Consider setting a “fun money” allowance

The goal is not to eliminate wants but to enjoy them responsibly.

VI. Step 4: Allocate 20% to Savings and Debt Repayment

This is where your financial future takes shape.

A. What This Category Includes

- Emergency fund

- Retirement savings

- Investments

- Extra debt payments (beyond minimums)

B. Prioritization Strategy

If you’re unsure where to start:

- Build an emergency fund

Aim for 3–6 months of living expenses - Pay off high-interest debt

Credit cards should be a top priority - Invest for the future

Retirement accounts and long-term investments

C. Automation Tips

Make saving easier by automating it:

- Set up automatic transfers to savings

- Contribute to retirement accounts through your employer

- Use apps that round up purchases

Automation removes the temptation to spend first.

VII. Putting It All Together

Let’s look at a sample budget using a monthly income of $3,500:

- Needs (50%) → $1,750

- Wants (30%) → $1,050

- Savings/Debt (20%) → $700

Example Breakdown

Needs:

- Rent: $1,000

- Utilities: $200

- Groceries: $300

- Transportation: $150

- Insurance: $100

Wants:

- Dining out: $300

- Entertainment: $200

- Shopping: $250

- Hobbies: $300

Savings/Debt:

- Emergency fund: $300

- Debt repayment: $200

- Investments: $200

Adjusting the Percentages

In real life, you may need to adjust:

- 60/20/20 for high-cost areas

- 50/20/30 if you’re aggressively saving

The rule is a guideline not a strict law.

VIII. Common Mistakes to Avoid

Even with a simple system, mistakes happen.

Misclassifying Wants as Needs

Be honest. Labeling luxuries as necessities defeats the purpose.

Ignoring Irregular Expenses

Expenses like:

- Annual subscriptions

- Car repairs

- Medical bills

Plan for these by setting aside money monthly.

Not Updating Your Budget

Your income and expenses change. Your budget should too.

Being Too Rigid

Life happens. Flexibility is key to long-term success.

Skipping Savings

Even if money is tight, try to save something even $10 matters.

IX. Tips for Sticking to Your Budget

Creating a budget is easy. Sticking to it is the real challenge.

Track Your Spending

Check in weekly to see where your money is going.

Use Tools

Apps or spreadsheets can make tracking easier and faster.

Set Realistic Goals

Avoid extreme restrictions they’re hard to maintain.

Build Flexibility

Allow room for unexpected expenses.

Celebrate Small Wins

Paid off a credit card? Saved your first $1,000? Acknowledge progress it keeps you motivated.

X. When the 50/30/20 Rule Might Not Work

While this rule is helpful, it’s not perfect for everyone.

Very Low Income

If your income barely covers essentials, focusing on percentages may not work.

High Debt

You may need to allocate more than 20% toward debt repayment.

Irregular Income

Freelancers or gig workers may need a more flexible approach based on fluctuating income.

Alternative Approaches

Other budgeting methods include:

- Zero-based budgeting

- Envelope system

- Pay-yourself-first strategy

Choose what fits your situation best.

XI. Conclusion

The 50/30/20 rule is one of the simplest and most effective ways to build a budget. It helps you balance your needs, enjoy your life, and plan for the future all without overwhelming complexity.

Let’s recap:

- Calculate your after-tax income

- Allocate 50% to needs

- Use 30% for wants

- Save or repay debt with 20%

Most importantly, remember that budgeting is not about perfection it’s about progress. Start where you are, make adjustments as needed, and keep moving forward.

Your next step: Take a few minutes today to calculate your income and map out your first 50/30/20 budget. The sooner you start, the sooner you’ll gain control of your finances.